The global automotive industry is experiencing a fundamental realignment driven by economic headwinds and shifting market dynamics. In Australia alone, new car sales reached 1,241,037 vehicles in 2025 with only marginal growth of 0.3 percent, while year-to-date sales through May 2026 declined by 0.7 percent, signaling persistent challenges across developed markets. High vehicle prices, elevated consumer debt levels, and constrained household budgets are dampening demand for big-ticket purchases worldwide.

Beyond immediate sales figures, the industry faces structural transformation as power dynamics shift between manufacturers, dealers, and consumers. Electric vehicles are gaining market share while traditional internal combustion engine sales stagnate, and China has emerged as a leading vehicle exporter, displacing Japan in key markets. These changes are forcing automakers and dealers to reconsider long-held strategies around inventory, pricing, and customer engagement.

The convergence of macroeconomic pressure and evolving buyer behavior is reshaping how vehicles are marketed, financed, and sold. Understanding these dual forces provides essential context for industry participants navigating an increasingly complex landscape where past assumptions about growth trajectories and consumer loyalty no longer hold.

Macroeconomic Drivers of Automotive Market Change

The automotive sector responds directly to shifts in inflation, financing conditions, and supply chain stability. These macroeconomic forces reshape production costs, consumer purchasing power, and inventory availability across global markets.

Inflation and Operating Costs

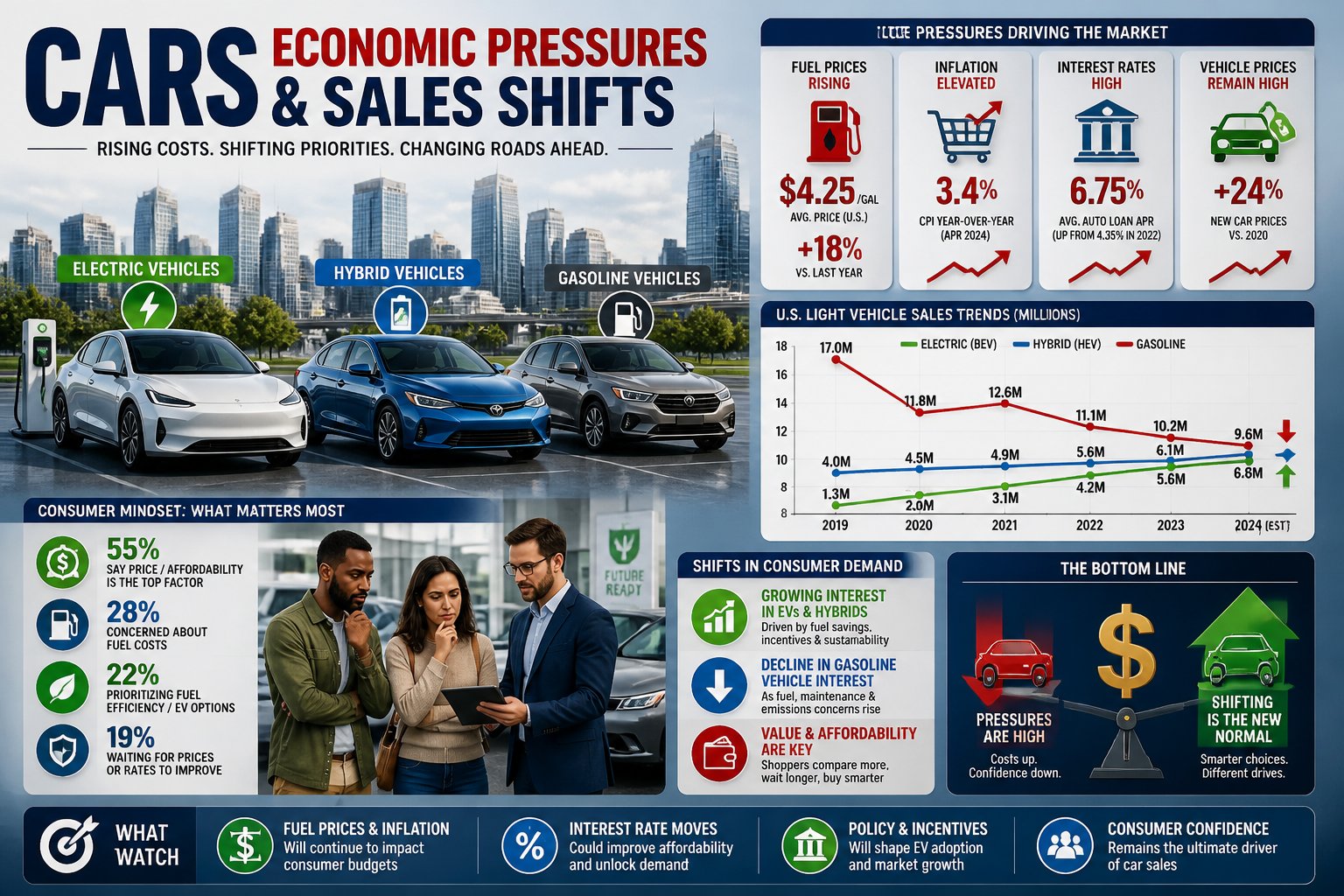

Rising inflation impacts both manufacturers and consumers through multiple channels. Production costs have increased substantially as raw materials, energy, and labor become more expensive. Steel, aluminum, and semiconductor prices remain elevated compared to pre-2020 levels, forcing automakers to absorb costs or pass them to buyers.

Vehicle prices have climbed accordingly. Average transaction prices for new vehicles in major markets remain 15-25% higher than three years ago. This pricing pressure reduces affordability for middle-income consumers, pushing some buyers toward used vehicles or delaying purchases entirely.

Operating expenses for dealerships and service centers also reflect inflationary pressures. Staff wages, facility maintenance, and parts inventory costs have risen, leading to higher service fees and financing margins that dealers must charge to maintain profitability.

Interest Rates and Consumer Financing

Central bank rate policies directly affect vehicle affordability through financing costs. Interest rates on auto loans in developed markets have doubled or tripled since 2021. A consumer financing a $35,000 vehicle now faces monthly payments $100-150 higher than during the low-rate environment.

Key financing impacts include:

- Extended loan terms stretching to 72-84 months as buyers seek lower monthly payments

- Increased lease costs reducing the appeal of leasing programs

- Higher subprime default rates among borrowers with weaker credit profiles

- Reduced transaction volumes in interest-sensitive market segments

These conditions particularly affect entry-level buyers and those purchasing premium vehicles. Cash purchases have gained market share where buyers possess sufficient liquidity.

Supply Chain Disruptions

Semiconductor shortages and logistics constraints continue affecting production schedules. While chip availability has improved from 2021-2022 lows, automakers still report constraints on specific components needed for advanced driver-assistance systems and infotainment features.

Regional supply chain variations create uneven production capacity. European manufacturers face energy cost pressures that Asian competitors avoid. North American plants benefit from nearshoring initiatives but contend with higher labor costs.

Inventory levels remain below historical norms in most markets. Dealers carry 30-40% less stock than pre-pandemic averages, limiting consumer choice and reducing price competition. Lead times for factory orders extend 8-16 weeks for popular models.

Evolving Consumer Preferences and Dealer Strategies

Dealerships face a market where buyers increasingly favor electric options, digital purchasing channels, and flexible pricing structures. Economic pressures have forced both consumers and dealers to rethink traditional sales approaches.

Shift Toward Electric and Hybrid Vehicles

Consumer interest in electric and hybrid vehicles continues to reshape inventory priorities at dealerships nationwide. Many buyers now consider fuel efficiency a primary factor in purchasing decisions, driven by volatile gas prices and environmental concerns.

Dealers are expanding their electric vehicle offerings while maintaining traditional ICE inventory to serve diverse customer segments. The bifurcated consumer market shows upper-income households embracing premium electric models, while budget-conscious buyers often opt for affordable hybrids or fuel-efficient conventional vehicles.

Key considerations for dealers include:

- Staff training on EV technology and charging infrastructure

- Installation of on-site charging stations to support test drives and customer education

- Partnership development with local utilities for customer incentive programs

- Extended service capabilities for battery maintenance and electric drivetrain repairs

The transition requires significant investment in training and infrastructure, but dealerships that adapt early position themselves to capture growing market share in electrified segments.

Adoption of Online Sales Models

Digital buying platforms have transformed how consumers research, compare, and purchase vehicles. Buyers now expect seamless online experiences that allow them to complete most or all of the purchasing process remotely.

Successful dealerships integrate digital tools with traditional showroom experiences rather than treating them as separate channels. Virtual inventory tours, online financing applications, and home delivery services have become standard expectations rather than premium features.

The shift demands robust digital infrastructure including real-time inventory systems, transparent pricing displays, and secure payment processing. Dealers must also maintain responsive customer service across multiple digital touchpoints while preserving the option for in-person interactions when buyers prefer them.

Inventory Management and Pricing Adjustments

Supply chain disruptions and changing demand patterns require dealers to adopt more agile inventory strategies. Many dealerships now carry leaner stock levels and utilize data analytics to predict which models will move quickly in their specific markets.

Pricing strategies have become more dynamic, with dealers adjusting markups based on real-time demand signals and local economic conditions. Lower-income consumers face affordability pressures that make certified pre-owned vehicles and extended financing terms increasingly attractive options.

Dealers benefit from diversifying their inventory mix to serve both premium and value-conscious segments. This includes stocking a range of vehicle types from entry-level sedans to luxury electric models, ensuring they capture sales across the economic spectrum rather than focusing exclusively on high-margin transactions.

{kind=link}